5 Best Crypto Business Loans List

The five platforms below are evaluated on collateral handling, pricing, and track record across the 2022 and 2024 market cycles:

- CoinRabbit: best for 10-minute access to funds and collateral security.

- Nexo: best for multi-asset business accounts.

- Ledn: best for Bitcoin-focused treasury financing.

- Arch Lending: best for high-net-worth and institutional borrowers.

- Maple Finance: best for on-chain institutional credit.

Crypto-backed credit has matured into a treasury tool for operating companies, mining firms, and family offices. A business holding Bitcoin or Ethereum on its balance sheet can borrow against that position without selling, preserving market exposure while accessing working capital.

The harder question is not whether to use a crypto loan, but which counterparty. After the 2022 collapses of Celsius, Voyager, and BlockFi, custody mechanics and rehypothecation policies sit at the center of institutional due diligence. Industry reporting puts more than $4 billion in customer funds at the center of those failures, much of it rehypothecated collateral pledged against active loans.

This article reviews five lending platforms for business use: CoinRabbit, Nexo, Ledn, Arch Lending, and Maple Finance. Each is assessed on collateral handling, LTV ceilings, APR, minimum loan size, and operational track record. Terms to know:

- LTV (loan-to-value): the loan amount as a percentage of collateral value.

- APR (annual percentage rate): the yearly cost of a loan including interest and fees.

- Margin call: a demand to add collateral when a price drop pushes LTV above a defined threshold.

- Rehypothecation: a lender’s practice of reusing pledged collateral by lending it out or trading against it for additional yield.

- Qualified custody: collateral held by a regulated trust company under segregated accounts, audited under SOC 1 or SOC 2 frameworks.

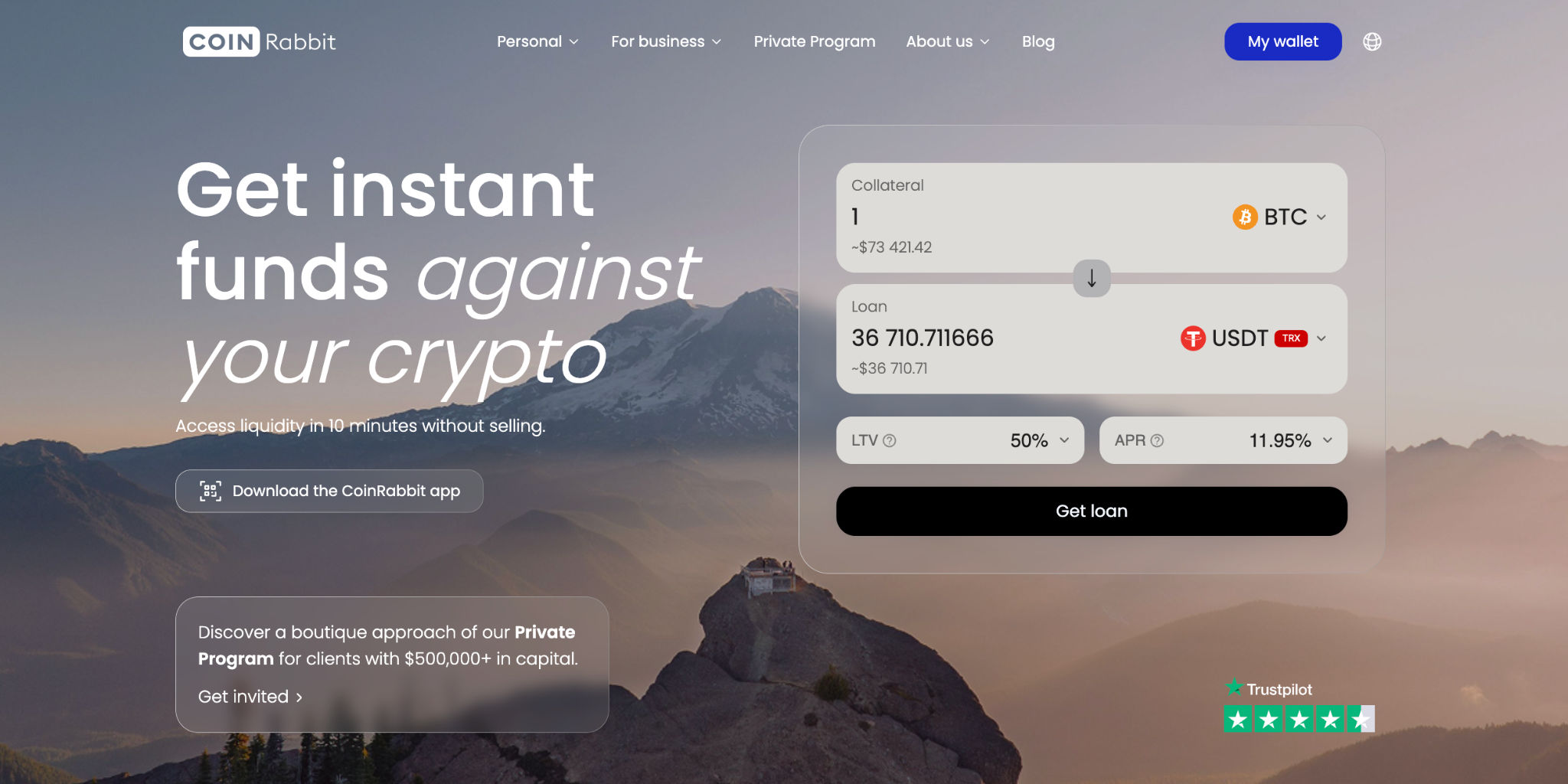

CoinRabbit – Best Crypto Business Loans for Collateral Security and 10-Minute Access to Funds

CoinRabbit is a security-first crypto asset management platform rather than a single-product crypto loan. The lending product gives businesses liquidity without selling assets, alongside instant settlement, stablecoin yield, and an in-platform exchange across 240+ tokens. Collateral is held in segregated cold wallets with multisig access and is never lent, traded, or pooled for internal yield. The platform reports a 100% capital reserve since inception, in contrast with the rehypothecation practices that produced the 2022 failures.

Key terms for business clients:

- No rehypothecation: collateral stays in cold storage under multisig keys, fully segregated from operating capital.

- Security: 100% capital reserve maintained since 2020.

- LTV range: 50% to 90%, set at origination.

- APR: starts from 11.95%, with interest paid at repayment rather than monthly.

- Collateral assets accepted: 350+, including BTC, ETH, SOL, XRP, and major stablecoins.

- Loan term: both limited and unlimited options.

- Support: 24/7 human support, not chatbot triage.

For larger balance sheets, the CoinRabbit Private Program serves portfolios above $500,000 with a dedicated relationship manager, cross-collateralization, and loan recovery option. The structure is built for family offices, treasury managers at crypto-native companies, and high-volume borrowers who need bespoke terms.

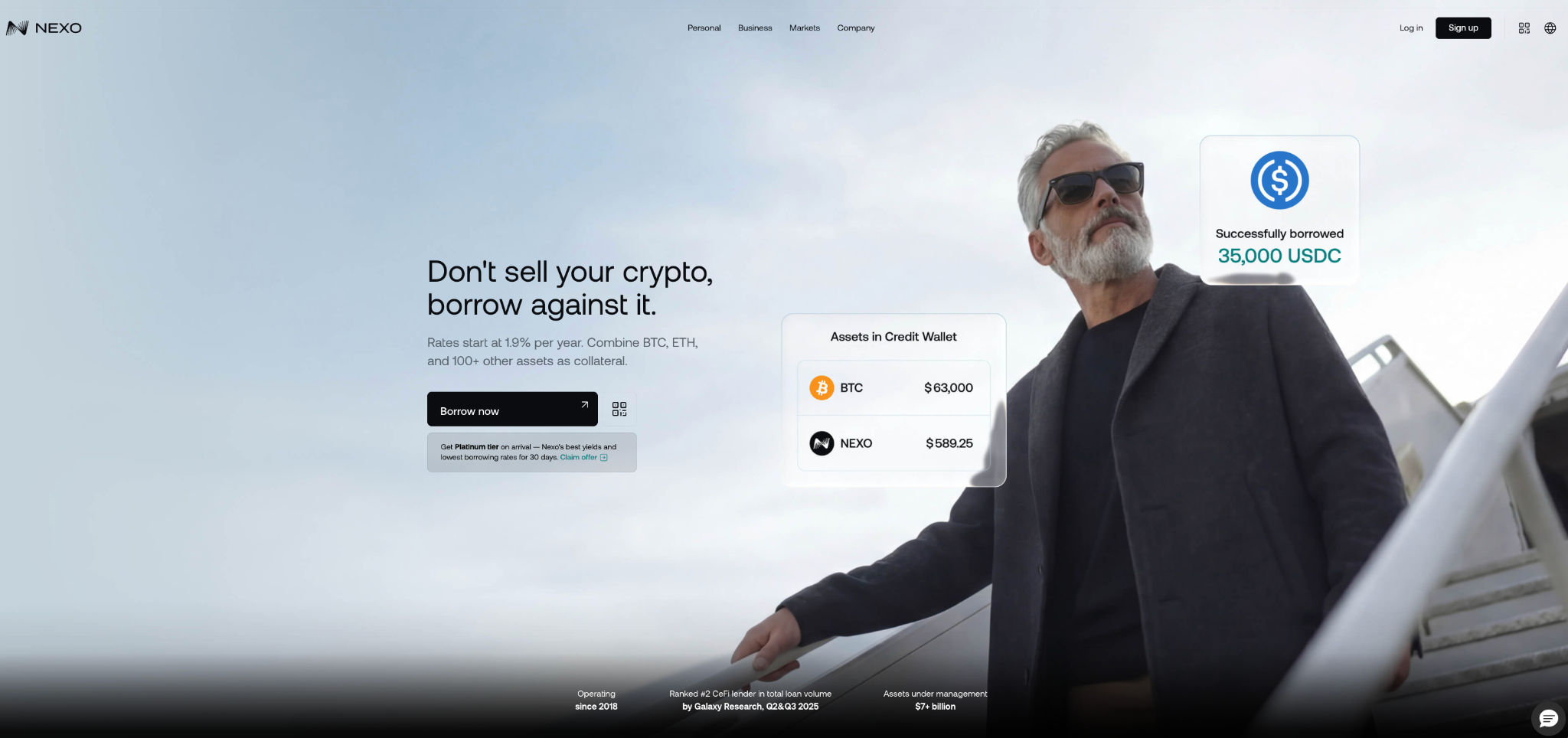

Nexo – Best Crypto Business Loans for Multi-Asset Treasury Access

Nexo runs one of the largest CeFi lending platforms by reported deposit base. Nexo Business targets corporate clients with loans collateralized against Bitcoin, Ethereum, stablecoins, and dozens of other assets.

Key terms for business clients:

- LTV: up to 50% for major assets, lower on higher-volatility tokens.

- APR: from 2.9% for the top loyalty tier (Platinum, holding NEXO tokens); standard-tier rates near 18.9%.

- Minimum loan: $1,000.

- Custody: assets held with qualified custodians including Ledger Enterprise Trust, BitGo Trust, and Fireblocks, per Nexo’s documentation.

- Insurance: Nexo cites $775 million in custodial insurance coverage through partners.

At the same time, Nexo can deploy client assets into lending markets to generate yield, a practice that meets the definition of rehypothecation. For business borrowers, this creates counterparty exposure on collateral even when the loan itself is current, because pledged assets may be moved into yield strategies during the loan term.

On the positive side, Nexo has proven resilient: it never paused customer withdrawals during the 2022 market turmoil. The platform enjoys strong user feedback (4.4–4.5 on Trustpilot), offers dedicated account managers, and delivers a convenient all-in-one solution with a Mastercard crypto card, OTC trading, and seamless fiat on/off-ramps. Its large scale reflects solid operational maturity and institutional trust.

This broad product suite is particularly useful for corporate workflows, although the rehypothecation model presents a different risk profile compared to lenders that do not re-use client collateral.

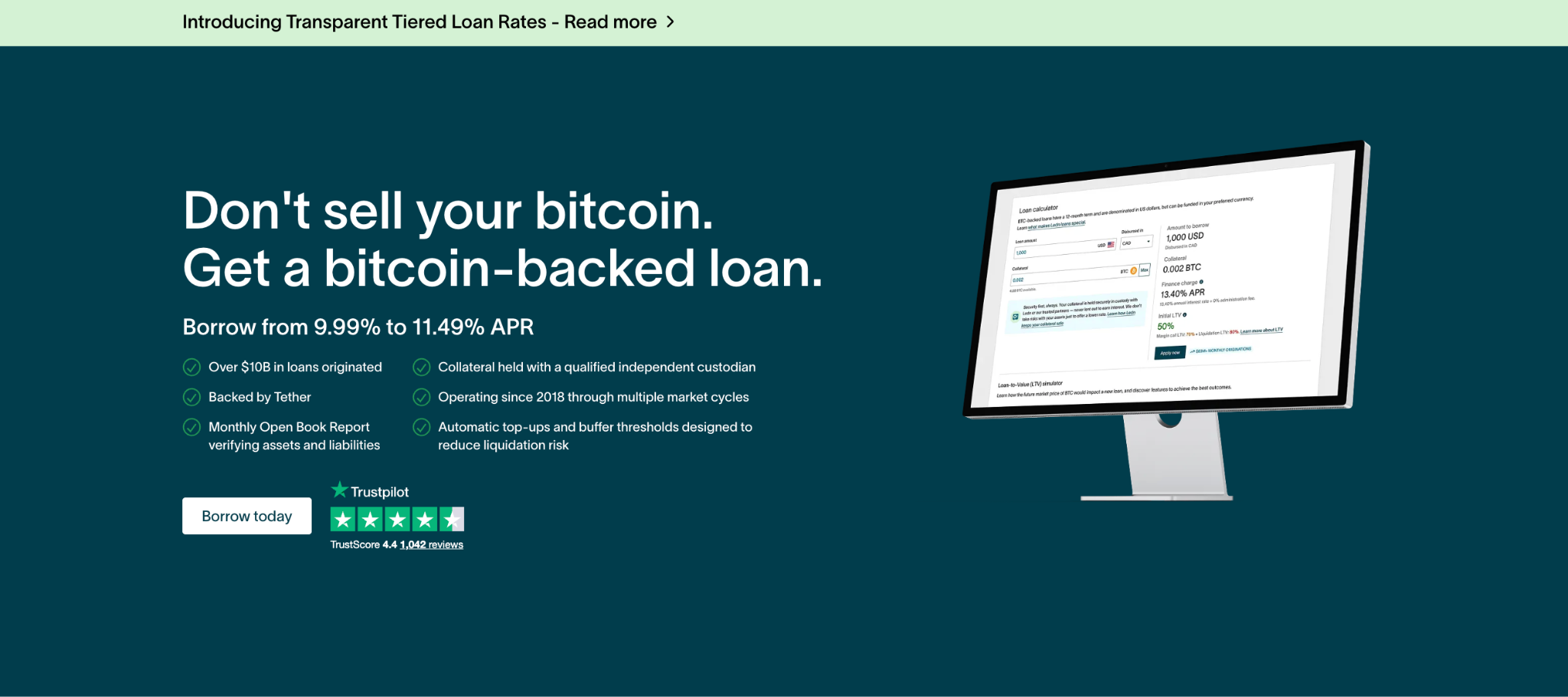

Ledn – Best Crypto Business Loans for Bitcoin-Focused Treasury

Ledn is based in the Cayman Islands, is a CeFi lender focused on Bitcoin and USDC credit. The platform serves retail and institutional borrowers and releases a semiannual Proof of Reserves attestation by Mariano LLC, one of the few CeFi lenders to do so publicly.

Key terms for business clients:

- Loan products: Ledn offers two tiers, “Custodied” (no rehypothecation, collateral at BitGo) and “Growth” (limited rehypothecation, lower rates).

- LTV: up to 50% at origination.

- APR: around 11.4% for Custodied loans; Growth loans priced lower.

- Minimum loan: $1,000 for retail; the institutional desk handles larger tickets directly.

- Collateral accepted: Bitcoin and Ethereum only.

Ledn’s Custodied tier keeps collateral fully segregated at BitGo Trust Company with no reuse, making it structurally similar to strict no-rehypothecation models. The Growth tier allows limited deployment of collateral into yield strategies, offering lower rates but introducing additional counterparty risk.

Business borrowers who prioritize custody can simply request the Custodied tier. The platform maintains strong user ratings (around 4.4 on Trustpilot), regularly publishes third-party audits, and provides dedicated institutional support with OTC settlement and tailored solutions. Its Bitcoin-focused approach enables tighter risk management, making it especially appealing to conservative corporate borrowers who value security and simplicity.

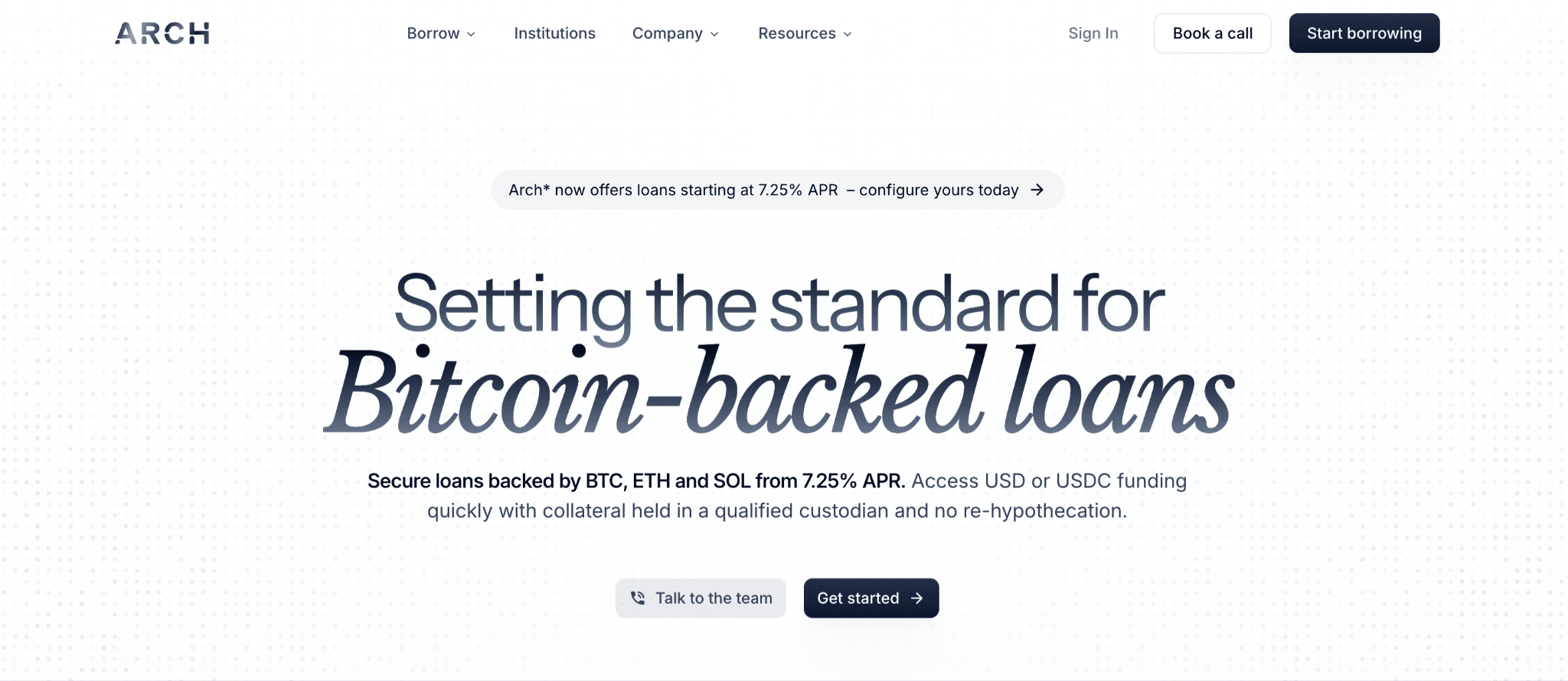

Arch Lending – Best Crypto Business Loans for Qualified Custody

Arch Lending is a U.S.-based crypto lender targeting high-net-worth individuals, family offices, and institutional borrowers. The platform is built around qualified custody and does not rehypothecate client collateral.

Key terms for business clients:

- Custody: collateral held with Anchorage Digital Bank, a federally chartered qualified custodian, in cold custody.

- No rehypothecation: collateral held one-to-one for each borrower in segregated accounts.

- LTV: up to 70% depending on asset and tenor.

- APR: from approximately 10.5%, depending on LTV and term.

- Minimum loan: $75,000, optimized for larger tickets.

- Collateral accepted: BTC, ETH, SOL, and select stablecoins.

Arch serves the institutional and HNW segment exclusively. The $75,000 minimum and qualified custody model are designed for treasury allocators rather than retail users, and margin calls are handled through documented procedures rather than algorithmic forced liquidation, a profile closer to a securities-backed line of credit.

The trade-off is reduced asset variety. Arch supports a narrower collateral list than CoinRabbit or Nexo and is not the right tool for diversified altcoin treasuries, but it offers a regulatory profile rare in the crypto credit market.

Maple Finance – Best Crypto Business Loans for On-Chain Institutional Credit

Maple Finance operates an on-chain credit infrastructure for institutional borrowers. The platform connects accredited lenders with vetted borrowers, including market makers, trading firms, and Bitcoin miners, through verifiable lending pools managed by external credit underwriters.

Key terms for business clients:

- Collateral: Bitcoin or stablecoins, set per pool.

- LTV: varies by pool, from overcollateralized retail-style loans to undercollateralized institutional credit lines.

- APR: pool-specific, ranging from approximately 8% to 14%, per Maple’s Q1 2026 pool disclosures.

- Minimum loan: $1 million floor, suited to institutional tickets.

- Pool delegates: institutional credit managers underwrite each borrower and set terms publicly on-chain.

Maple’s structure differs from CeFi lenders: collateral in each pool is locked to that pool’s smart contract rather than commingled with platform balances, which reduces the rehypothecation surface compared with CeFi lenders that mix client assets with operating capital. Pool composition, borrower exposure, and historical default data are verifiable in real time on-chain.

The platform survived the 2022 contagion that took down Celsius, BlockFi, and Voyager because each lending pool was structurally isolated. The trade-off is that origination involves application, KYB, and credit underwriting, which makes Maple a fit for established firms rather than treasury teams seeking fast loans against existing holdings.

How to Choose the Right Crypto Business Loans Provider for Your Company

The strongest selection criterion for a business crypto loan is the custody arrangement. After 2022, treasury teams treat rehypothecation as a primary counterparty risk: when a lender reuses pledged collateral, that collateral can be lost even if the borrower is current on every payment. The 2023 SEC action against Genesis and Gemini showed how quickly customer assets become entangled when commingled with operating capital.

Five criteria worth weighing in any provider review:

- Custody and rehypothecation policy. Confirm in writing whether collateral sits in segregated cold storage with multisig access and whether the lender publishes an explicit no-rehypothecation policy.

- Regulatory and audit posture. Look for Proof of Reserves attestations, third-party qualified custody (BitGo, Anchorage, Fidelity Digital Assets), and SOC 1 or SOC 2 reporting.

- Pricing clarity. Verify the headline APR, origination fees, and accrual method. CoinRabbit charges interest at repayment with no monthly outflow; several competitors compound monthly.

- Asset coverage. A BTC-only treasury has different needs than a portfolio with twenty altcoins. CoinRabbit accepts 350+ assets, Ledn supports only BTC and ETH, Arch covers a select institutional list.

- Service tier and support. For tickets above $500,000, a dedicated relationship manager and proactive margin alerts (offered through CoinRabbit’s Private Program) reduce operational risk during volatility events.

The contract is the source of truth. Several platforms describe segregated custody in marketing copy but route smaller balances through omnibus accounts in practice. Request the actual custody chain in writing before signing.

How Crypto Business Loans Improve Capital Efficiency

A crypto-backed business loan converts an illiquid balance sheet asset into working capital without forcing a sale. For a mining firm holding 500 BTC at roughly $100,000 per coin, a 70% LTV loan releases approximately $35 million in stablecoin liquidity, leaves the underlying position intact, and does not trigger a capital gains event.

The capital efficiency mechanics:

- Avoidance of taxable disposal: in most jurisdictions, including the U.S. under IRS Notice 2014-21, a loan against an asset is not a taxable event, while a sale of crypto triggers capital gains. Local tax counsel should confirm jurisdiction-specific treatment.

- Preserved upside: collateral continues to appreciate during the loan term, and any gain accrues to the borrower at repayment.

- No credit check: most crypto lenders, including CoinRabbit, do not pull credit or report to credit bureaus, since the loan is fully secured by digital collateral.

- Flexible deployment: funds support operating expenses, payroll, equipment, or expansion without diluting equity or selling reserves.

The risk to manage is price drawdown. A 40% drop in collateral value at 70% LTV triggers a margin call, and businesses should plan for top-up capital or partial repayment ahead of any extended downturn. CoinRabbit’s Private Program addresses this with proactive alerts, and the no-rehypothecation policy ensures the borrower’s collateral remains recoverable upon repayment.

Conclusion

For businesses evaluating crypto-backed credit, the counterparty question matters more than the headline rate. The 2022 collapses showed that rehypothecation can impair borrower collateral even when the loan itself is performing.

Of the five platforms reviewed, CoinRabbit, Ledn’s Custodied tier, and Arch Lending offer the clearest no-rehypothecation models. CoinRabbit’s combination of cold-wallet multisig custody, 100% capital reserve since 2020, and a Private Program for portfolios above $500,000 makes it the strongest fit where collateral security ranks alongside speed.