Since launching 12 years ago, Bankless Times has brought unbiased news and leading comparison in the crypto & financial markets. Our articles and guides are based on high quality, fact checked research with our readers best interests at heart, and we seek to apply our vigorous journalistic standards to all of our efforts.

BanklessTimes.com is dedicated to helping customers learn more about trading, investing and the future of finance. We accept commission from some of the providers on our site, and this may affect where they are positioned on our lists. This affiliate advertising model allows us to continue providing content to our readers for free. Our reviews are not influenced by this and are impartial. You can find out more about our business model here.

How and Where to Buy Bitcoin in 2025

In 2024, Bitcoin managed to surpass $100K, sparking market-wide optimism. More recently, Cathie Wood predicted that the crypto could reach $600K in 2030 – a new golden target that could provide excellent returns to early adopters. If you’re looking to buy Bitcoin before it reaches it’s next all-time-high, here is a complete guide on how to buy Bitcoin in 2025.

In this guide, we cover how to buy Bitcoin from major exchanges such as Coinbase and eToro. We also take a look at best practices for staying safe when buying Bitcoin as well as how to decide which purchasing method is best for you.

How to Buy Bitcoin in 2025 – Step by Step

If you are comfortable with cryptocurrency and want to get started quickly, here is a basic overview of how to buy Bitcoin from an exchange. For more information, keep reading through our guide.

- Choose an exchange: Research different exchanges to find the most suitable platform for your needs. Look for platforms with low fees, a friendly interface and robust security measures.

- Create and fund your account: Register using your email or phone number. Then, connect a payment method to your account to deposit funds.

- Search for BTC: Search for Bitcoin in the platform’s explore dashboard and select Bitcoin, or ‘BTC’. Be wary of derivative options that may be available on some exchanges.

- Buy Bitcoin with fiat currency: Open a ‘BUY’ order and use your account balance to buy Bitcoin. It will appear in your account after a few minutes.

- Send your Bitcoin to a wallet: Create a Bitcoin wallet (your exchange may offer one) and send your Bitcoin to your address for safe keeping.

Where To Buy Bitcoin in 2025

There are a range of options available to investors looking to buy bitcoin in 2025. Below, I’ve broken down some of the best options in more detail.

| Platform | Fees | Regulation | Mobile App | Cryptocurrencies Offered | Minimum Deposit |

| Coinbase | 0.5% – 4.5% | Financial Crimes Enforcement Network (FinCEN) and OFAC. Coinbase is also regulated by governing bodies in 45 different US jurisdictions. | Yes | 240+ | $10 |

| Revolut | 0% – 0.09% | Revolut is not regulated in the US for crypto trading. | Yes | 175+ | Specific to each currency |

| Robinhood | 0% commission (fees are charged using a variable spread) | U.S. Securities and Exchange Commission (SEC) and Financial Industry Regulatory Authority (FINRA).Robinhood is also regulated by governing bodies in 31 different US jurisdictions. | Yes | 15+ | No minimum deposit |

| eToro | 0% commission (fees are charged using a variable spread) | Financial Crimes Enforcement Network (FinCEN). eToro also holds Money Transmitter Licenses (MTLs). | Yes | 100+ | $100 |

1. Coinbase – The best centralized exchange to buy Bitcoin

Coinbase is one of the most popular platforms for buying Bitcoin. It is a highly regulated, well-trusted centralized exchange that allows you to buy, sell, send, receive and store BTC.

Coinbase is a very beginner-friendly platform that makes it relatively easy to buy Bitcoin and more than 240 other crypto assets.

You can also store your BTC on the Coinbase platform or transfer your holdings to the Coinbase Wallet for safekeeping.

- A platform well suited for new cryptocurrency investors

- An excellent range of cryptocurrencies on offer

- Transparent fee structure

- Better suited for long-term investors rather than short-term traders

- Relatively weak customer support

- High fees compared to other centralized exchanges

2. Revolut – The best mobile app to invest in Bitcoin

Revolut is an app-based cryptocurrency exchange that allows you to buy Bitcoin and more than 175 other cryptocurrencies. It is also possible to send and receive BTC, as well as over 30 other crypto assets, using Revolut.

The Revolut app is well-designed and is available to both Android and iOS users. It isn’t possible to buy Bitcoin on the desktop version of the site.

Revolut charges as little as $0 per Bitcoin transaction, depending on your account level. You can also set up a recurring buy which will automatically buy a set amount of BTC on a weekly/monthly basis.

Finally, Revolut X is a specialist platform that advanced traders can use to gain access to a range of advanced trading tools and analytics.

- It’s possible to buy bitcoin with zero fees

- The Revolut app is very user-friendly

- Revolut X gives you the chance to utilize advanced trading tools

- It’s difficult to transfer cryptocurrencies outside of the Revolut app

- Platform is not available to US customers

- Not possible to buy bitcoin without the app

3. Robinhood – Buy Bitcoin with zero commission

Robinhood is arguably the best platform for buying Bitcoin with low fees. Although Robinhood offers less than 20 cryptocurrencies, you can invest in bitcoin with $0 commission.

The platform makes it fairly straightforward to send and receive BTC to and from a self-custodial cryptocurrency wallet. It is also quite a user-friendly platform that also offers advanced trading tools for more experienced traders.

You can enjoy 24/7 customer support with Robinhood, and buy bitcoin using the Robinhood app on both Apple and Android devices.

- Commission-free bitcoin trading

- Responsive, 24/7 customer support available

- Advanced trading tools offered to more experienced traders

- Very few other cryptocurrencies offered

- The platform is not very beginner-friendly compared to other exchanges and brokers

- Limited educational options available

4. eToro – Buy Bitcoin spot ETFs

eToro is a beginner-friendly platform that prioritizes building a strong trading community. It is a social trading and investing platform that allows you to copy the portfolio of more experienced traders using the site’s unique CopyTrader™ feature.

You can trade over 6,000 assets, including bitcoin and more than 100 other cryptocurrencies, on eToro. Unlike most other cryptocurrency exchanges, eToro also allows you to invest in bitcoin ETFs.

You can send BTC and other cryptocurrencies to the eToro Money crypto wallet for safe storage. It’s also possible to earn staking rewards on some crypto assets, although this is not available for Bitcoin.

For beginner investors, the eToro Academy offers a range of educational materials. It’s possible to find articles about blockchain technology, buying Bitcoin, and other, non-crypto specific topics.

eToro USA LLC and eToro USA Securities Inc.; Investing involves risk, including loss of principal; Not a recommendation. eToro USA LLC does not offer CFDs. Crypto investing carries a high risk and is highly volatile. eToro (Europe) Ltd crypto trading is provided via DLT Finance, crypto custody by Tangany. Tax may apply.

- Very beginner-friendly platform that prioritizes social trading and investing

- Offers bitcoin ETFs

- The eToro Money wallet lets you store bitcoin securely

- Customer support leaves a little to be desired

- eToro fees work using a “variable spread”, which can be a little confusing

- You cannot send BTC back to eToro once it’s in your eToro Money wallet

How to Buy Bitcoin (BTC): Step-by-Step

Follow the below step-by-step guide to learn exactly how to buy Bitcoin from a centralized exchange.

Step 1: Sign up to an exchange

Once you’ve chosen the exchange you want to use to invest in Bitcoin, you’ll need to create an account. Centralized exchanges will require you to input your personal information and follow the relevant Know Your Customer (KYC) checks. These are a legal requirement and will often involve you submitting a photo of your ID, alongside a photo of your face.

You may also need to answer some questions about your trading and investing knowledge, as well as your risk tolerance. This is to ensure the exchange doesn’t offer you products that aren’t suitable for your experience level.

Step 2: Fund your account

Fund your account by following the specific processes on your chosen exchange. Usually, there will be a fairly obvious “Deposit” or “Add Funds” button. Choose from one of the offered payment methods and deposit an amount of your preferred fiat currency.

Remember to account for any fees, as well as any minimum deposit or purchase requirements.

Step 3: Conduct research and create a strategy

Before you start buying Bitcoin, make sure to do thorough research and create a comprehensive investment strategy. Don’t rush into buying BTC because lots of people are talking about it; this is often a sign that the price of Bitcoin is becoming over-inflated.

Think about your long-term investment goals and aversion to risk. Know how much money you’re hoping to make and avoid investing emotionally when the price of BTC rises or falls. Be aware of the wider cryptocurrency market, potential regulatory changes and the broader geopolitical climate – all of these things can impact the price of Bitcoin.

Step 4: Search for BTC

Once you’re ready to buy bitcoin, search for “BTC” or “bitcoin” in your exchange’s navigation bar. Alternatively, bitcoin will usually be the first option available on a cryptocurrency exchange.

Clicking on this will often open up a specific “Bitcoin (BTC)” market page.

Step 5: Buy bitcoin

Buy bitcoin by choosing the amount of BTC you wish to purchase, or how much fiat currency you want to spend. Choose your payment method or use the funds that you deposited earlier.

Review your transaction before proceeding. The exchange will highlight any fees you’ll be charged for making the purchase and tell you exactly how much bitcoin you’ll receive.

Step 6: Transfer your bitcoin to a crypto wallet

Once the transaction is complete, consider transferring your BTC to a crypto wallet for safekeeping. Some exchanges will have built-in storage solutions, but it’s usually better to use a self-custodial wallet.

A cold wallet is an online storage solution that is encrypted using a private key. A hot wallet is an offline, physical storage option that provides additional security but makes it more difficult to actively trade your bitcoin.

How to Sell Bitcoin

If you decide to sell your Bitcoin, you’ll need to transfer it back to the cryptocurrency exchange from your wallet. Use the address provided by the exchange, but be aware that you may be charged a fee for making this transaction.

Once your Bitcoin is back on the exchange, follow the platform’s process for selling it. This will usually involve navigating to your list of assets, clicking “Sell” and deciding how much of your bitcoin you want to get rid of.

Make sure that you’re happy with the price being offered, as well as any potential fees, and then confirm the transaction.

How to Buy Bitcoin with PayPal

Some investors will want to buy crypto with PayPal. This is usually fairly straightforward, although not every exchange will accept the payment method. Coinbase is one example of an exchange that accepts PayPal transactions.

Once you’ve found an exchange that accepts PayPal, visit their “Deposit” page. Select “PayPal” as a payment method and decide how much of your chosen fiat currency you want to deposit. Once the funds have been added, visit the “Bitcoin (BTC)” market page and buy BTC as you would normally.

Alternatively, you can often buy Bitcoin with PayPal directly. When you click “Buy”, choose PayPal as your preferred payment method and follow the on-screen instructions to make your Bitcoin purchase.

How to Buy Bitcoin with a Credit Card

It’s fairly common for investors to use a credit card to buy Bitcoin. Most platforms, including eToro, will accept it as a payment method, but just double-check that your preferred exchange does.

Use your credit card to add funds to your account by heading to the “Deposit” page and choosing “Credit Card”. Add your required funds by inputting the amount of fiat currency you wish to deposit to your account. Once the funds have cleared, visit the “Bitcoin (BTC)” market page and buy Bitcoin with the funds that you’ve added.

You can also usually buy BTC by choosing “Credit Card” as an option on the Bitcoin “Buy” page.

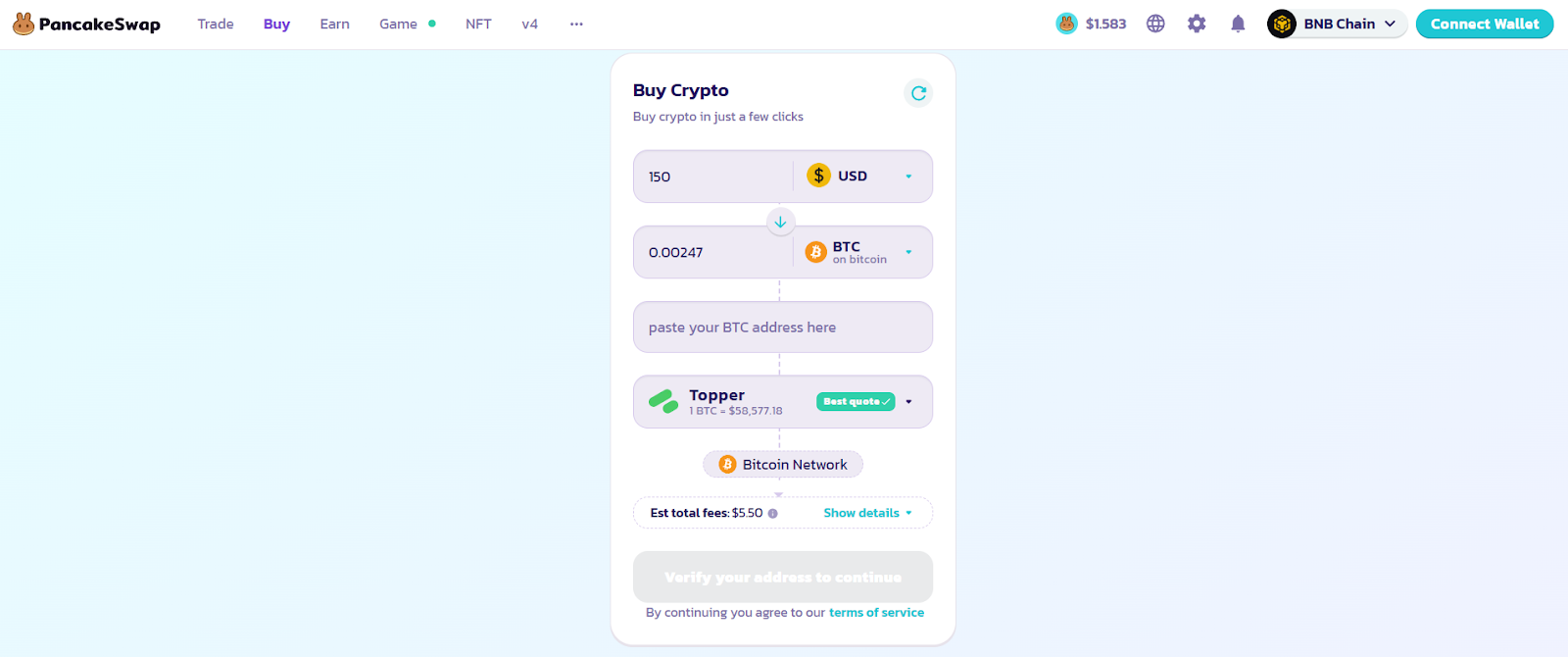

Buying Bitcoin Through a Peer-to-Peer Exchange

A peer-to-peer (or decentralized) exchange is a marketplace for buying and selling bitcoin, and other cryptocurrencies. The “decentralized” nature of the process means that there are no central or third-party intermediaries involved in the process, which is why some investors prefer using decentralized exchanges (DEX).

To buy Bitcoin on a peer-to-peer exchange, first make sure that the platform offers it. For the most part, a DEX will only offer cryptocurrencies that are compatible with the blockchain that the exchange is built on. However, a lot of these exchanges will also offer bitcoin. For example, PancakeSwap, a decentralized exchange built on the BNB Chain, allows you to buy BTC.

Decide how you want to buy Bitcoin on your chosen DEX; this could involve swapping Bitcoin for another cryptocurrency or buying it with fiat currency. You will need to create a cryptocurrency wallet in order to buy Bitcoin using a peer-to-peer exchange.

Make sure you’ve selected “Bitcoin (BTC)” and that you’ve added in your Bitcoin wallet address. Keep an eye on any fees – these often fluctuate when using a decentralized exchange – and confirm the transaction. You may need to wait a little while before your new Bitcoin appears in your wallet, but don’t worry, this is perfectly normal.

Bitcoin ATMs

A Bitcoin ATM (or BTM) works in the same way as a standard ATM. It is a physical kiosk, owned and operated by third-party providers, that allows you to buy Bitcoin.

Insert cash or a debit/credit card and swap your fiat currency for bitcoin. You’ll first need to have an account with the provider and ensure you’ve verified your identity. Make sure you have a Bitcoin-compatible wallet for your new Bitcoin to be sent to.

There are thousands of Bitcoin ATMs dotted around the world, although the majority of them can be found in the US.

Top Tips for Buying Bitcoin Safely

As with any cryptocurrency purchase, it’s important to remain safe when buying Bitcoin. Here are some top tips for buying Bitcoin safely in 2025.

1. Always conduct research and analysis

Conduct thorough research before you start investing. Make sure you understand exactly how the cryptocurrency market works and at which stage in the four-year cycle Bitcoin is currently in.

Keep an eye on the wider geopolitical climate and be aware of any regulatory changes that might impact the price of Bitcoin.

Always have a strategy before you start investing. Set realistic investment goals and understand your investment time horizon.

2. Don’t invest more than you can afford to lose

As with any investment, buying Bitcoin is not a guarantee that you will make money. Crypto is an incredibly volatile asset class and it’s perfectly possible that the value of BTC could drop more than 20% in a single day.

Assume that your bitcoin holdings will fall significantly in value – how would this make you feel? If this would leave you in financial difficulty, then you’re investing too much!

Consider investing small amounts more frequently, rather than committing a huge sum of money to a single trade.

3. Use a reputable exchange

Always use a reputable exchange to buy Bitcoin. If you’re using a centralized exchange, make sure that it is licensed and regulated. If you’re using a decentralized exchange, make sure you understand how it works and look at user reviews to see whether other investors have had a positive experience with it.

H3: 4. Store your coins in a cold wallet

Once you’ve purchased your Bitcoin, consider storing it in a cold wallet. This is a physical, offline storage solution (similar to a memory stick) that will keep your Bitcoin safe from malicious attacks.

Important Things to Know About Bitcoin

- Between March and June 2025, Goldman Sachs purchased $418 million worth of bitcoin ETFs. Of this amount, $238 million was spent on shares of BlackRock’s iShares Bitcoin Trust.

- Recent research suggests that bitcoin does not actually qualify as a “real currency”. In a chapter in the Second Edition of the Handbook of Digital Currency, David Yermack suggests that bitcoin often fails to meet the criteria of a real currency: a medium of exchange, unit of account and store of value.

- In January 2025, Cathie Wood, Ark Invest Management’s CEO and Chief Investment Officer, suggested that bitcoin could reach a price of $600K by 2030.

Final Thoughts

Bitcoin is not only one of the world’s most popular cryptocurrencies, it is quickly becoming one of the world’s most popular assets in general. It is therefore essential that you understand exactly how to buy Bitcoin.

Always do your research and find a platform that you’re comfortable using. Consider using a centralized exchange for a more straightforward process or a decentralized exchange for greater security and lower fees.

Store your Bitcoin safely using a cold wallet once you’ve bought it. Alternatively, if you’re going to be trading your Bitcoin more actively, there are some good hot wallet solutions that will allow you to do so, while still keeping your BTC secure.

FAQs

How can a beginner invest in Bitcoin?

A beginner can invest in bitcoin by creating an account with a reputable centralized exchange. Verify your identity, deposit funds into your new account and visit the “Bitcoin (BTC)” market page. Decide how much bitcoin you want to buy and confirm the transaction.

What is the cheapest way to buy Bitcoin?

Find an exchange that offers lower fees. For example, Robinhood allows you to invest with $0 commission, which means that it might be cheaper than an exchange that charges fees for making a purchase.

Decentralized, peer-to-peer exchanges are also sometimes cheaper than centralized exchanges because they work using an automated system of smart contracts.

Is it worth buying bitcoin?

Many investors believe it to be worth buying bitcoin because of its huge upside potential. However, it is a very volatile asset and could quickly lose a large percentage of its value. Consider real-world use cases for bitcoin and how likely it is to be adopted by the general population, large corporations and financial institutions.

Related Crypto Guides

Contributors